“Do not invest blindly, but invest with knowledge, experience and confidence. Only then will you be successful.”

– Nicholas Sergio

Happy New Year to all. 2021 is officially in the record books and, to most investors’ surprise, it turned out to be a good year. As we reflect on the past 18 months, we all have a lot to be thankful for. We have an economy on strong footing, low unemployment, minimum wages rising (that’s a very good thing) and a country that likely will be moving from a pandemic stage to endemic stage. As I sit and pencil this Quarterly Insights installment, my primary goal as always, is to help educate our investors and provide insights about the current investing landscape and where I believe it’s very likely heading. Unlike typical business news commentary, we do not intend to create anxiety for our clients but rather give them a sense of understanding of their investments, and be a reliable source of knowledge through both the good and challenging times. On behalf of the entire Banyan Wealth team, thank you for dedicating time out of your busy lives to read and listen to our advice – we are truly grateful. Each and every day, we appreciate the opportunity to play such an important part of your life and never take it for granted.

Periods of Instability Create Periods of Stability; Periods of Stability Often Create Periods of Instability

As we wrote in April of 2020, periods of instability often lead to periods of stability. This was especially true in 2021 with the S&P 500 having experienced no more than a 6% peak to trough drawdown as compared to an average secular bull market drawdown of 8% to 12%.

Source: FactSet

I would anticipate the investors’ honeymoon with stability to start showing some fracturing as we head into and through 2022. The Volatility Index (commonly referred to as the VIX) started to display some manic behavior in 2021 with multiple spikes up and down, this type of behavior in the VIX can often lead to larger, more typical drawdowns in the equity markets. Basically, with a pending tightening cycle to begin most likely in the first half of 2022, it is easy to assume that we will see a greater degree of volatility and price fluctuations in equity markets in the first several quarters of 2022.

Source: FactSet

Negative Real Interest Rates

Negative real interest rates are the federal funds rate less core inflation and by definition mean that inflation is higher than interest rates. As a result, savers will see a fall in the real value of their savings. When this rate is negative, which it is currently, their tends to be a positive correlation with the positive equity markets.

Bank of America High Yield Option Adjusted Spread

This index, which basically measures the perceived risk of default in the high yield bond market, recently traded to new lows in spread. These are pre-pandemic lows and reinforce that the outlook for corporate credit is strong.

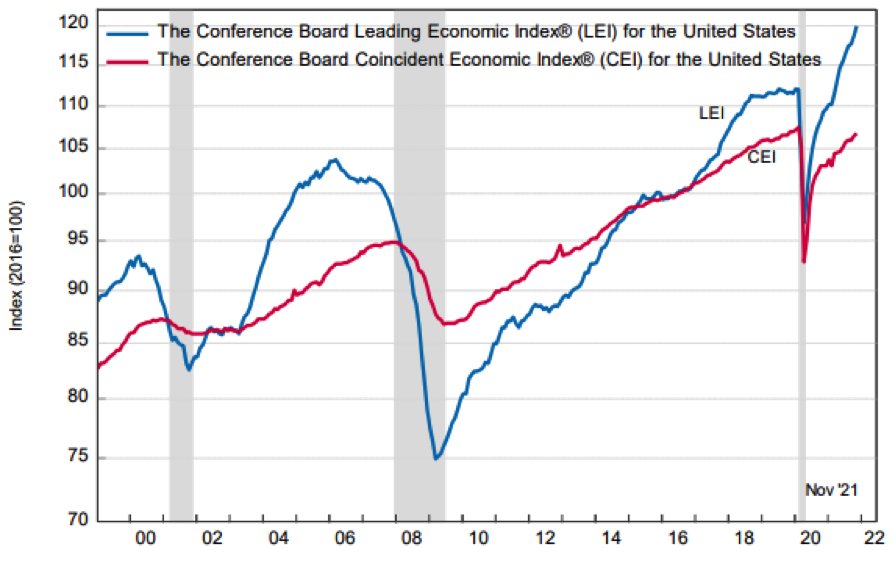

The Economy and Recession 2022

The Conference Board Leading Economic Index (LEI) and Coincident Economic Index (CEI) both hit new cycle highs in the month on November. These new highs are a sign that the US economy is healthy despite all the inflation fears that are currently present.

Source: The Conference Board

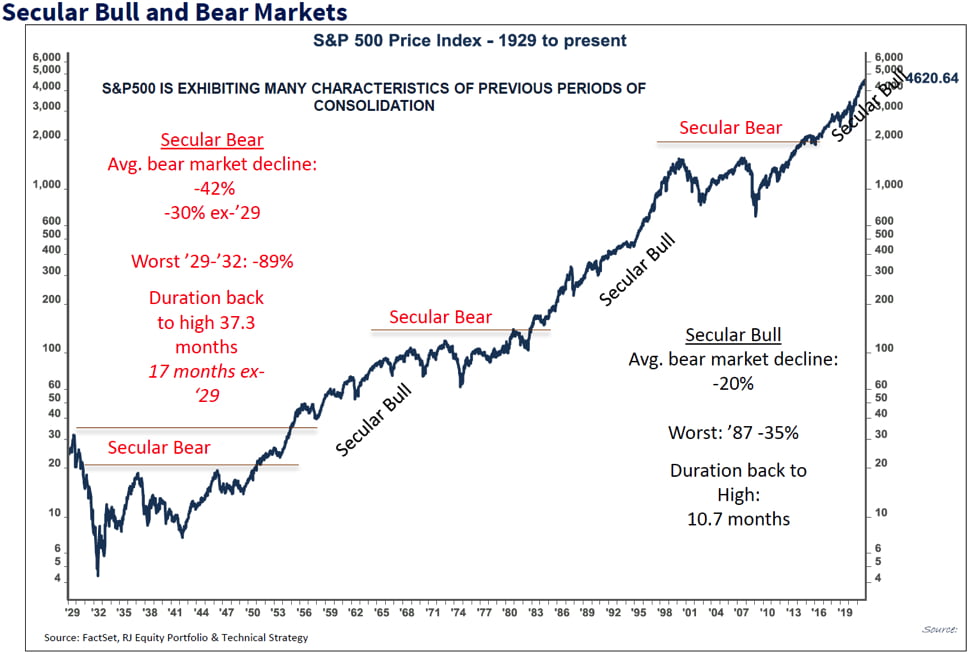

Secular Bull Market

In closing, we believe the secular bull market still has years to run and should reward those with patience and a longer-term investment horizon. In the upcoming year, we feel confident that the Federal Reserve will begin a tightening cycle by raising short-term interest rates. This higher initial interest rate move has a tendency to create a short-term negative reaction in the equity markets. However, in the longer term and as history has shown, the equity markets tend to react positively to this tightening cycle. With this being said, I would anticipate a short-term increase in market volatility and price fluctuations.