2021 Second Quarter Insights

The 4 Rules of Investing

1. “Investing is a marathon and not a sprint.”

2. “Do no harm.”

3. “Knowledge creates success; stay calm, objective and long-term oriented.”

4. “Choose carefully what you read and to whom you listen.”

“Today’s a good day. Tomorrow will be better.”

– Nicholas Sergio

In many ways, the events of 2020 are both significantly different and identical to the Great Recession of 2008-2009. The major contrast is that the Great Recession was a structural event with massive wealth destruction, while the 2020 Pandemic was a transitory event leaving our economy and U.S. families with greater financial health and strength. On behalf of the entire Banyan Wealth team, thank you to all of our valued clients for the opportunity to play such an important role in your lives as we begin our return to normalcy. As we begin this transition, we hope you spend this time with your family and friends, catching up on those missed doctor’s appointments and simply returning to living the life you love.

COVID Recovery

One year ago, the S&P 500 had bottomed after the fastest 34% correction in its history. A year later and over 550,000 lives lost to Covid-19, we find ourselves on a fast track to recovery. Signaling a broad-based rebound in hiring, March non-farm payrolls rose by 916,000 and the unemployment rate dropped to 6%, down from a COVID high of 14.8% in April 2020. Household balance sheets are in great shape with net assets growing to $122.9 trillion from the end of 2019 pre-pandemic levels of $114 trillion. Low interest rates, an accommodative Federal Reserve and a big move from city life to the suburbs is also adding to the recovery in a big way. Factories around the world are struggling to keep up with demand, supply chains are strained as workers are being hired back, furloughed factories are reopening and the hardest hit industries (hospitality and leisure for instance) are hiring workers back at a strong pace. There will be some bumps in the recovery and it won’t be balanced for everyone. However, the combination of an accommodative Federal Reserve and President Biden’s pressing down of the accelerator pedal with his Covid Relief Bill – stimulus checks being deposited in people’s bank accounts and his proposed $2.0 trillion American Jobs Plan package – the recovery could move faster than most would have thought possible only 12 months ago.

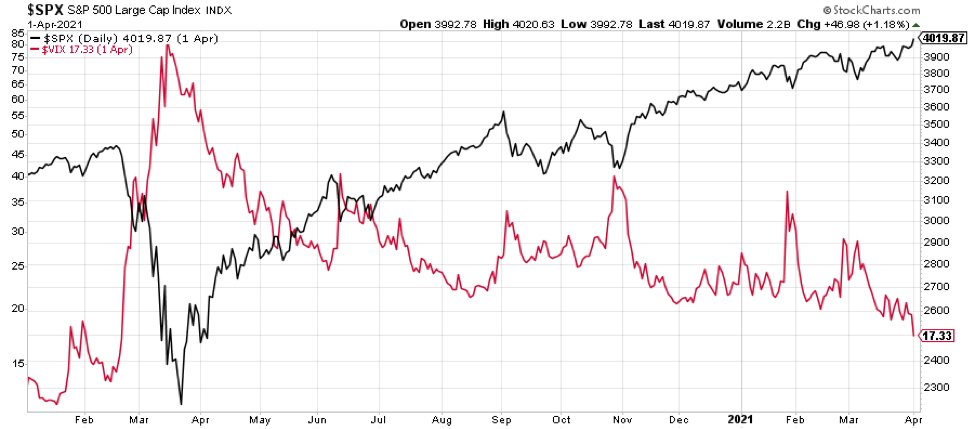

Periods of Increased Instability Create Periods of Stability

During the large shocks to the economy and financial markets in 2020, we saw the Volatility Index spike to an extreme high of 85. Those spikes corresponded with a 34% drop in the S&P 500. Since the bottom in March of 2020, we have seen the Volatility Index return to levels seen pre-pandemic and the S&P 500 tag all-time highs. Generally, a falling or low Volatility Index is beneficial for equity prices. In the chart below, the Volatility Index is red and the S&P 500 is black.

Source: StockCharts.com

Dow Theory Buy Signal

In January, we registered another Dow Theory Buy Signal with the Dow Jones Industrial Average hitting all-time highs concurrently with the Dow Jones Transportation Index also registering all-time highs. This is a healthy sign for higher prices in the intermediate to longer-term time frames.

Source: StockCharts.com

Interest Rates and Equity Prices

Recently, we have experienced a rise in interest rates, specifically in the 5, 7 and 10-year Treasuries. Investors in growth stocks seem to have been spooked by such an interest rate rise. There is investor speculation that the U.S. Economy is on the verge of rapid inflation and the Federal Reserve is going to be forced to raise interest rates sooner and faster than anticipated. Our view is that any short-term rise in inflation will be mostly transitory based upon the rapid reopening of our economy and the desire for Americans to return back to more normal lives. We will also note that slowly rising interest rates are not necessarily a bad thing for equity prices. During the 1992 – 2000 time frame, the Federal Reserve and Alan Greenspan raised interest rates and the S&P 500 rose nearly 300%.

In Closing

With the events that have occurred over the last 12 months, my opinion remains unchanged – the Secular Bull market will continue to roll on for many years as we are in a long-dated Secular Bull Market that was reset during 2020.

Be well, be safe and live the life you love.

Nicholas W. Sergio, AIF®

Founder & Chief Investment Officer • Banyan Wealth

Registered Principal & Financial Advisor • RJFS

2021 RJFS Leaders Council Member*

The S&P 500 is an unmanaged index of 500 widely held stocks that is generally considered representative of the U.S. stock market. The NASDAQ composite is an unmanaged index of securities traded on the NASDAQ system. Dow Jones Industrial Average (DJIA) commonly known as “The Dow” is an index representing 30 stocks of companies maintained and reviewed by the editors of the Wall Street Journal. The Russell 2000 Index measures the performance of the 2000 smallest companies in the Russel 3000 Index, which represents approximately 8% of the total market capitalization of the Russel 3000 Index. BPS stands for Basis Points and refers to a common unity of measure for interest rates, one basis point is equal to 1/100th of 1% or 0.01% it is used to denote the percentage change in a financial instrument. Inclusion of these indexes is for illustrative purposes only. Keep in mind that individuals cannot invest directly in any index, and index performance does not include transaction costs or other fees, which will affect actual investment performance. Individual investor's results will vary. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of capital might occur. All investing involves risk and you may incur a profit or loss of capital. There is no assurance any investment strategy will be successful. All information, data and analysis provided in this report is for informational purposes only and is not a recommendation to buy or sell any security. This report does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual clients. The foregoing information has been obtained from sources considered to be reliable, but we do not guarantee that it is accurate or complete; it is not a statement of all available data necessary for making an investment decision and it does not constitute a recommendation. Any opinions are those of Nicholas Sergio and not necessarily those of Raymond James and are subject to change without notice. Raymond James does not offer tax advice and services. You should discuss any tax matters with the appropriate professional. Holding investments for the long term does not insure a profitable outcome. There is no guarantee that these statements, opinions or forecasts provided herein will prove to be correct. Forward looking data is subject to change at any time and there is no assurance that projections will be realized. High-yield bonds are not suitable for all investors. The risk of default may increase due to changes in the issuer’s credit quality. Price changes may occur due to changes in interest rates and the liquidity of the bond. When appropriate, these bonds should only comprise a modest portion of a portfolio. Investment advisory services offered through Raymond James Financial Services Advisors, Inc.

* Membership is based on prior fiscal year production. Re-qualification is required annually. The ranking may not be representative of any one client’s experience, is not an endorsement, and is not indicative of advisor’s future performance. No fee is paid in exchange for this award/rating.

https://www.investopedia.com/terms/v/vix.asp

https://www.investopedia.com/terms/d/dowtheory.asp

https://www.investopedia.com/terms/s/sp500.asp

https://www.investopedia.com/terms/1/10-yeartreasury.asp

... See MoreSee Less

0 CommentsComment on Facebook

The S&P 500's 50-day overbought streak since 1943 raises flags. While AI innovation and low unemployment offer promise, soaring oil prices and sticky inflation remain concerns. Read more in Nick's second insight of 2024. #banyanwealth #raymondjamesredbank www.raymondjamesconnect.com/a0tlDd ... See MoreSee Less

0 CommentsComment on Facebook

... See MoreSee Less

0 CommentsComment on Facebook

As the first quarter of 2024 is ticking away, let’s pause and reflect on the importance of staying ahead in our financial journey. I’m approaching 2024 with caution, prepared for the bumpy roads and potential opportunities ahead. Dive into our Q1 insights to ensure your financial strategy is as resilient and adaptable as you. Take a look: ... See MoreSee Less

0 CommentsComment on Facebook

... See MoreSee Less

0 CommentsComment on Facebook